Most people only ever see the surface of insurance. You buy a policy. You pay a premium. If something goes wrong, you file a claim and expect to be paid.

What you never see is what makes that promise believable.

Behind every insurance policy sits a second layer of capital and contracts that absorbs losses when things go wrong. That layer is called reinsurance. It is the financial system that keeps insurance from collapsing when bad years happen.

This post walks through how reinsurance works using the same flow shown in Re’s Reinsurance Basics deck.

The Risk Supply Chain

At the top of the system are the things people insure: cars, homes, health, businesses, and catastrophes.

Those risks flow into primary insurance companies. These are the insurers you recognize. They collect premiums and promise to pay claims.

But insurers do not keep all of that risk.

A portion of every policy flows down into a reinsurer. The insurer sends part of the premium, and the reinsurer agrees to pay part of the losses if claims occur. In other words, insurers buy insurance for themselves.

The reinsurer then spreads that risk even further into other reinsurers and capital markets. This creates very large pools of capital that sit behind the entire insurance system.

This is why insurance works. Risk and money keep getting pushed outward into bigger, more diversified pools.

Crypto people already understand this pattern. Liquidity pools, risk pools, and yield all come from the same place: capital absorbing uncertainty.

Reinsurance is the institutional version of that.

Why Risk Is Shared

Insurance is volatile. Some losses happen all the time but cost little. Others happen rarely but cost a lot. Sometimes many losses happen at once.

Reinsurers exist to smooth that volatility.

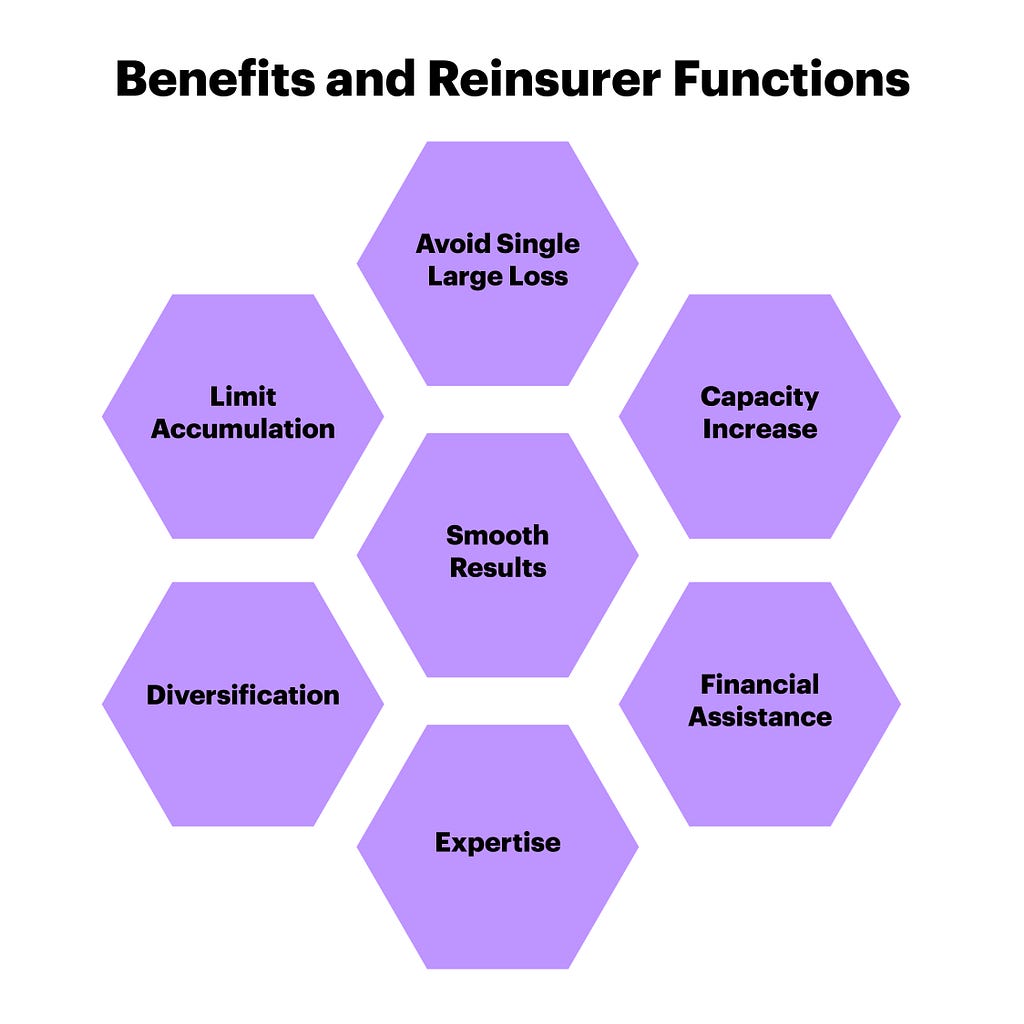

By transferring risk, insurers get:

- protection from large single losses

- more stable financial results

- the ability to write more policies

- access to expertise and diversification

In simple terms, reinsurance turns wild, spiky cashflows into something stable and predictable. That is what allows insurers to grow without blowing up.

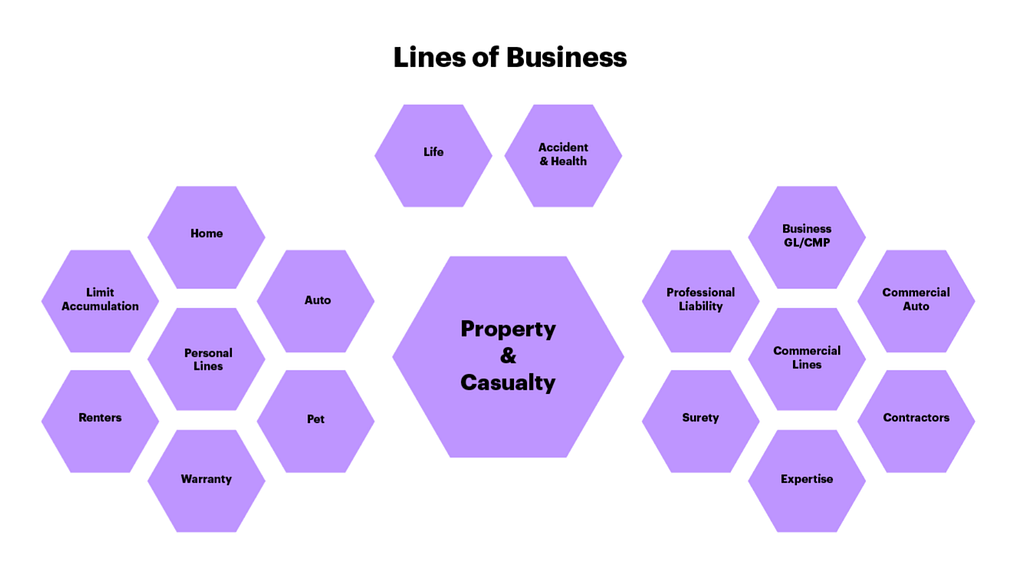

What Kind of Risk Exists

Insurance does not cover one thing. It covers many.

There is life and health, homes and renters, cars and shipping, businesses, contractors, and workers.

Each type of risk behaves differently. Some have frequent small claims. Others have rare but massive ones. Reinsurance allows all of these to be blended into portfolios so no single company is exposed to too much of any one outcome.

How Reinsurance Is Sold

There are two main ways insurers transfer risk.

Treaty reinsurance is bulk coverage. A whole portfolio of similar policies is covered under one agreement. If a policy fits the criteria, it is automatically included. This is like a pooled market.

Facultative reinsurance is one-off. A single large or unusual policy is negotiated on its own. This is like a bespoke OTC deal.

Both exist because risk does not come in one uniform shape.

How Losses Are Shared

There are two main ways premiums and losses are split.

In proportional structures, the insurer and reinsurer split premiums and losses by percentage. If the reinsurer takes 50 percent of the business, it gets 50 percent of the premium and pays 50 percent of the claims.

In excess of loss structures, the insurer keeps the first layer of losses and the reinsurer only pays after losses pass a certain point. This creates layers of risk. Small losses stay with the insurer. Big losses move to the reinsurer.

If this sounds like tranches, that is because it is.

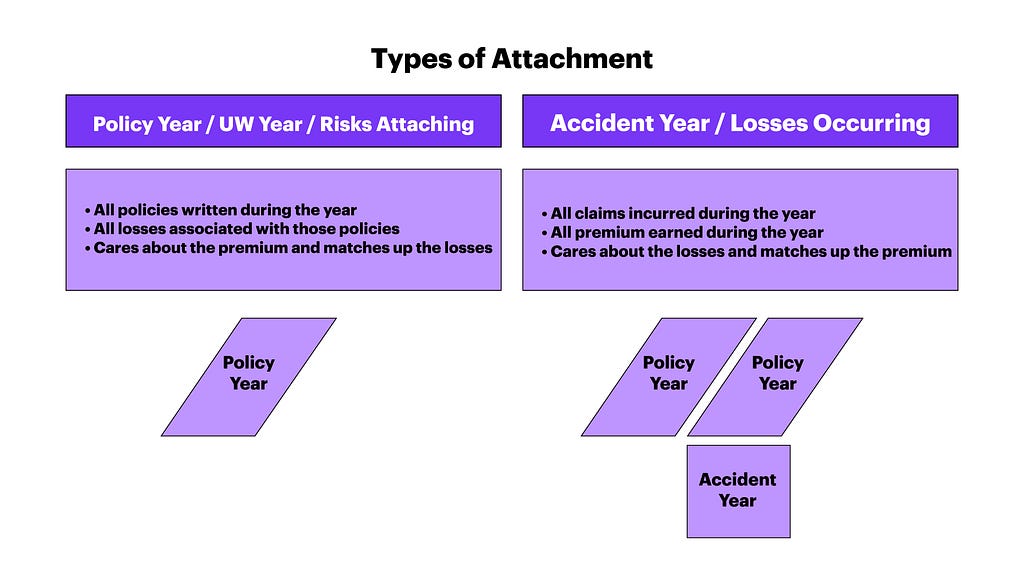

When Losses Count

Insurance runs on time.

Premiums are earned slowly. Claims can arrive years later. Reinsurance contracts define how those two timelines line up.

Some contracts track losses based on when events happen. Others track losses based on when policies were written. This ensures that premiums and claims are matched properly even when cashflows are spread over long periods.

Where Re Fits

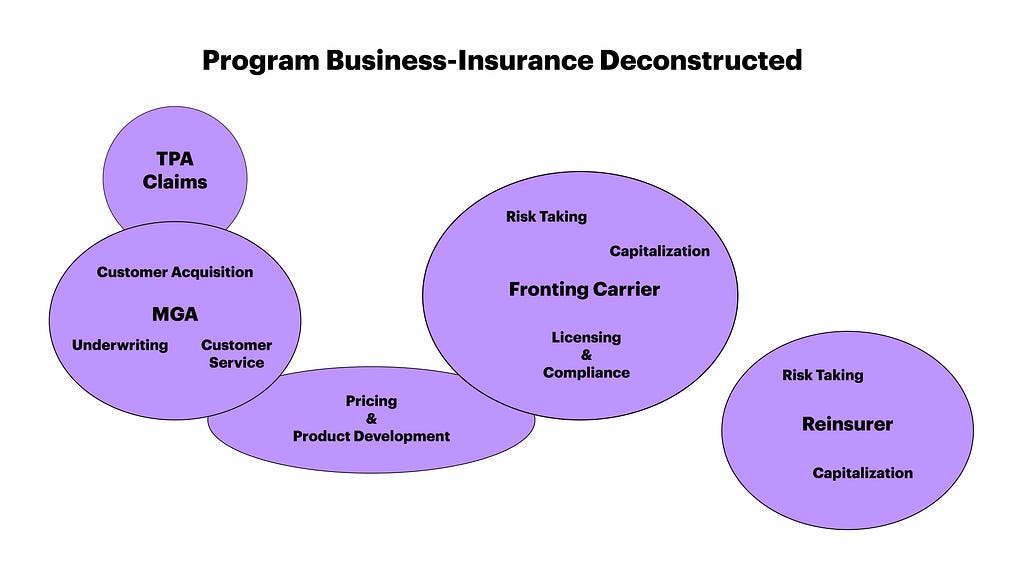

In a traditional insurance company, one firm does everything: selling, underwriting, claims, compliance, and capital.

Modern insurance is modular. One company handles customers. Another handles claims. Another provides licenses. Another supplies capital and takes risk.

Reinsurance is the capital and risk layer of that stack.

Re brings that layer onchain.

Instead of reinsurance being negotiated privately between institutions, Re structures and manages reinsurance exposure using smart contracts. Onchain capital can now play the same role that traditional reinsurers play: absorbing defined insurance risk in exchange for premium-based returns.

The risks are real. The premiums are real. The difference is that the capital, the accounting, and the exposure are transparent and programmable.

Why This Matters

Reinsurance is one of the quiet reasons modern life works. It is why insurers survive disasters. It is why premiums do not explode after every bad year. It is why long-term promises remain credible.

By moving reinsurance onchain, Re turns a closed institutional market into open financial infrastructure.

This is not a new kind of insurance.

It is the same system that has existed for centuries.

It is simply becoming visible, composable, and accessible to crypto capital.

And that is what makes it powerful.