The State of the Reinsurance Market at Year-End 2025 — And How Re Is Navigating It

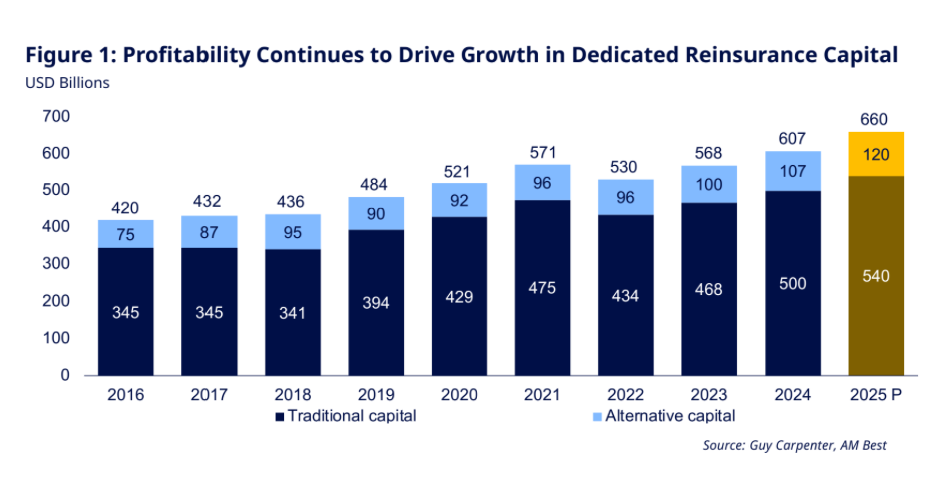

In 2025, the reinsurance market grew significantly in size, but returns became more constrained.

A major driver of that growth was the catastrophe bond market. Catastrophe bonds, or “cat bonds,” are securities that allow insurers and reinsurers to transfer large disaster risks, such as hurricanes, earthquakes, and wildfires, to capital market investors. These bonds are typically issued under Rule 144A, a U.S. securities framework designed for institutional buyers. In practice, this results in large deal sizes, standardized structures, and long issuance cycles. Cat bonds work well for peak property catastrophe risk where losses are well modeled, and portfolios are large.

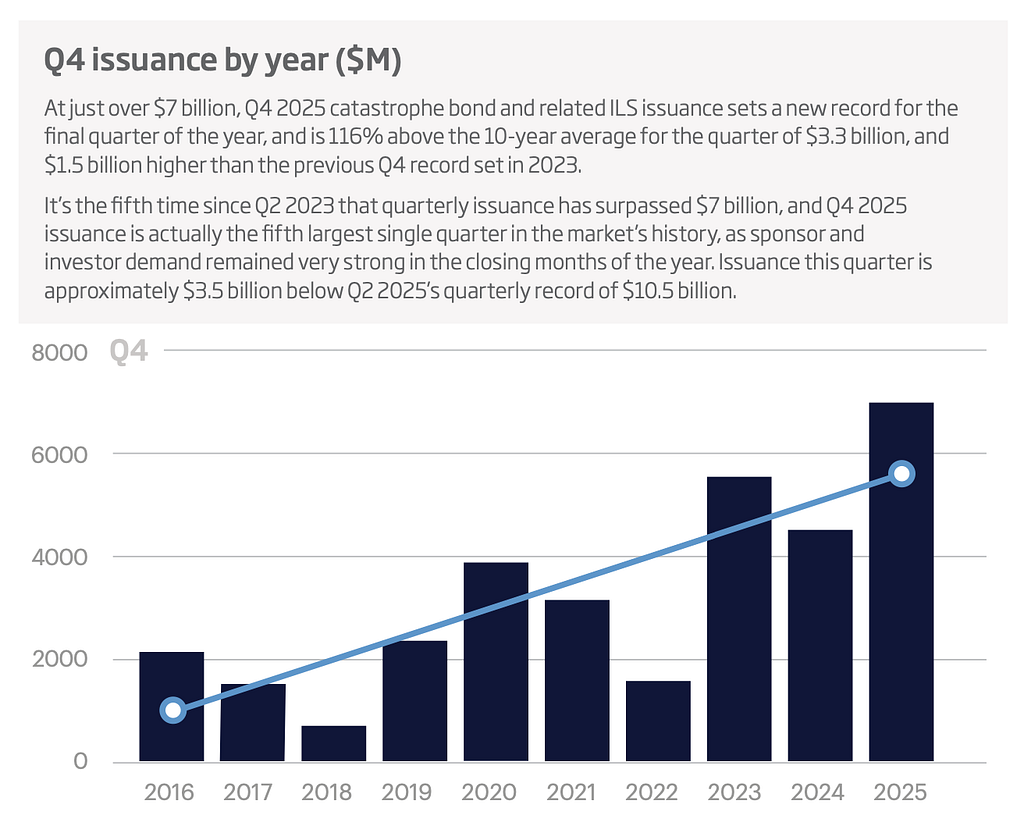

In 2025, cat bond issuance reached a record of $25.6 billion, increasing the outstanding market to over $60 billion. Nearly all of this issuance was concentrated in traditional 144A property catastrophe bonds. Capital flowed in, more sponsors entered the market, and demand routinely pushed deal sizes higher during marketing. At the same time, yields are compressed. Spreads fell, pricing tightened, and risk multiples declined as competition increased. The market became deeper and more liquid, but also more efficient and less forgiving.

This is not a failure of the cat bond market. It is a sign of maturity. Where risk is standardized and capital is abundant, returns converge.

Outside of public cat bonds sits a much smaller but important segment: private insurance-linked securities, often referred to as private ILS or “cat bond lite” transactions. These structures are used for smaller, more flexible reinsurance placements that are not well suited to public issuance. They allow for lower minimums, customized risk profiles, and faster execution, but they are less liquid and more operationally intensive.

Despite growing demand, private ILS issuance totaled only about $626 million in 2025, a small fraction of the public cat bond market. This gap reflects a structural reality: many risks are too small, too complex, or too dynamic for public markets, yet too operationally demanding for large reinsurers focused on balance-sheet efficiency.

Not all parts of the reinsurance market improved as capital expanded. Specialty and non-catastrophe lines remain unevenly served. Loss volatility persists. Underwriting discipline still matters. Some risks warrant being constrained or avoided altogether. Growth alone does not eliminate complexity.

These observations are necessarily broad and apply unevenly across the industry. Property catastrophe risk, in particular, is where competition, capital intensity, and yield compression are most pronounced. Re’s exposure to property risk is intentionally limited. Where Re does participate, it does so selectively and with conservative structures.

On the casualty side, the largest uncertainties tend to sit in mid-market to large-account business with high limits, often $10 million and above. These portfolios are more exposed to social inflation, class actions, and the type of large verdicts that drive outsized losses. Re’s underwriting focus is different. The majority of its exposure is to smaller, “main street” risks, such as the average American small business, with lower limits typically in the $1–2 million range. These risks historically attract fewer class-action dynamics and are less exposed to the tail-loss behavior seen in large-account casualty books.

This is the environment Re is operating in.

At year-end, Re has nearly $400 million in total value locked across the protocol, calculated as the sum of on-chain capital, off-chain capital, and premiums receivable. That growth reflects demand for reinsurance capacity, but it does not come from chasing the most crowded parts of the market or relying on standardized catastrophe exposure.

Re focuses on underwriting profit first. Capital is allocated selectively, pacing matters, and not every opportunity is pursued. Some risks are priced conservatively. Others are passed on entirely.

Reinsurance markets move in cycles. Not every environment is ideal, and not every year offers the same opportunities. This is expected. Re is structured to remain resilient through changing market conditions, prioritizing disciplined underwriting and capital deployment over short-term optimization.

(Below is reframed as a quote from Karn)

As Re CEO, Karn Saroya notes:

“Reinsurance is cyclical by nature — some years are simply better set up for opportunity than others. That is expected. Re is built to stay durable across market turns, staying disciplined on underwriting and capital deployment instead of chasing short-term optimization.”